Quick Guide: Understanding US Credit Scores in 2025 (and How to Improve Yours). Your credit score is one of the most important numbers in your financial life. Whether you’re applying for a credit card, car loan, mortgage, or even renting an apartment, lenders and businesses use this score to decide how trustworthy you are with money. In 2025, credit scoring models are smarter and more dynamic than ever, but the basics still remain the same.

What Is a Credit Score?

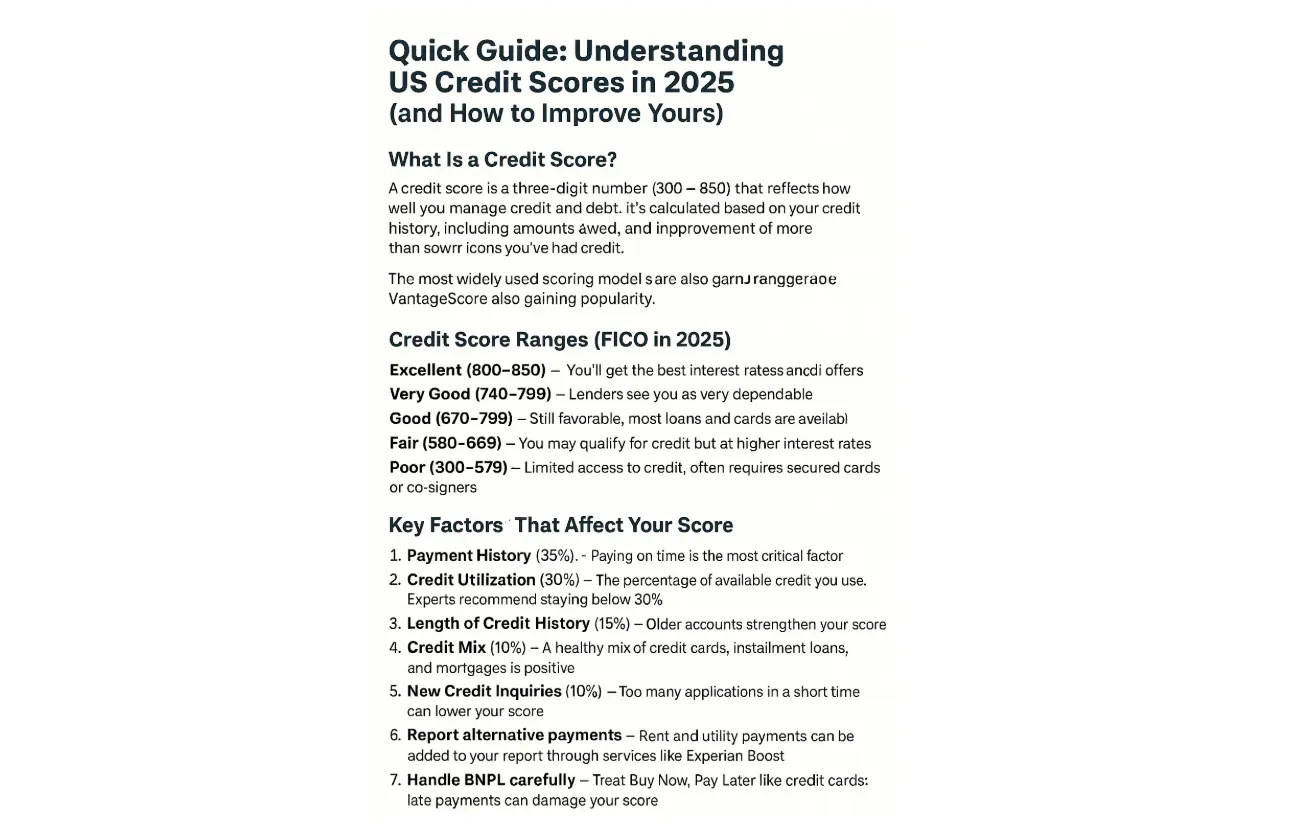

A credit score is a three-digit number (300–850) that reflects how well you manage credit and debt. It’s calculated based on your credit history, including how much you owe, how often you pay bills on time, and how long you’ve had credit.

The most widely used scoring model is the FICO Score, but VantageScore is also gaining popularity.

Credit Score Ranges (FICO in 2025)

- Excellent (800–850): You’ll get the best interest rates and credit offers.

- Very Good (740–799): Lenders see you as very dependable.

- Good (670–739): Still favorable, most loans and cards are available.

- Fair (580–669): You may qualify for credit but at higher interest rates.

- Poor (300–579): Limited access to credit, often requires secured cards or co-signers.

Key Factors That Affect Your Score

- Payment History (35%) – Paying on time is the most critical factor.

- Credit Utilization (30%) – The percentage of available credit you use. Experts recommend staying below 30%.

- Length of Credit History (15%) – Older accounts strengthen your score.

- Credit Mix (10%) – A healthy mix of credit cards, installment loans, and mortgages is positive.

- New Credit Inquiries (10%) – Too many applications in a short time can lower your score.

What’s New in 2025?

- AI-driven credit models: Lenders are using more advanced algorithms that consider rental payments, utility bills, and even subscription services if reported.

- Buy Now, Pay Later (BNPL) accounts: Many BNPL services are now being reported to credit bureaus, which can help or hurt your score depending on usage.

- Medical debt changes: Small medical debts under $500 are no longer included in most credit reports, easing pressure on millions of Americans.

How to Improve Your Credit Score in 2025

- Pay bills on time, every time – Set up autopay or reminders.

- Keep utilization low – If your card limit is $10,000, try not to use more than $3,000.

- Avoid closing old accounts – Even if unused, they help with credit history length.

- Limit hard inquiries – Apply for new credit only when needed.

- Check your credit reports regularly – Use AnnualCreditReport.com for free reports.

- Report alternative payments – Rent and utility payments can be added to your report through services like Experian Boost.

- Handle BNPL carefully – Treat Buy Now, Pay Later like credit cards; late payments can damage your score.

Why Your Credit Score Matters

- Determines loan approvals and interest rates.

- Affects insurance premiums in some states.

- Can influence whether you get approved for renting an apartment.

- Impacts your ability to start a business with financing.

In 2025, building and maintaining a good credit score is less about tricks and more about consistent, responsible money habits. Pay on time, borrow wisely, and monitor your reports. A strong credit score not only saves money but also opens the door to better financial opportunities.

#CreditScore #CreditTips #Finance2025 #MoneyMatters #SmartMoney #PersonalFinance

← Reference Sheet: US Tax Brackets 2025 Explained in Simple Terms

Leave a Reply